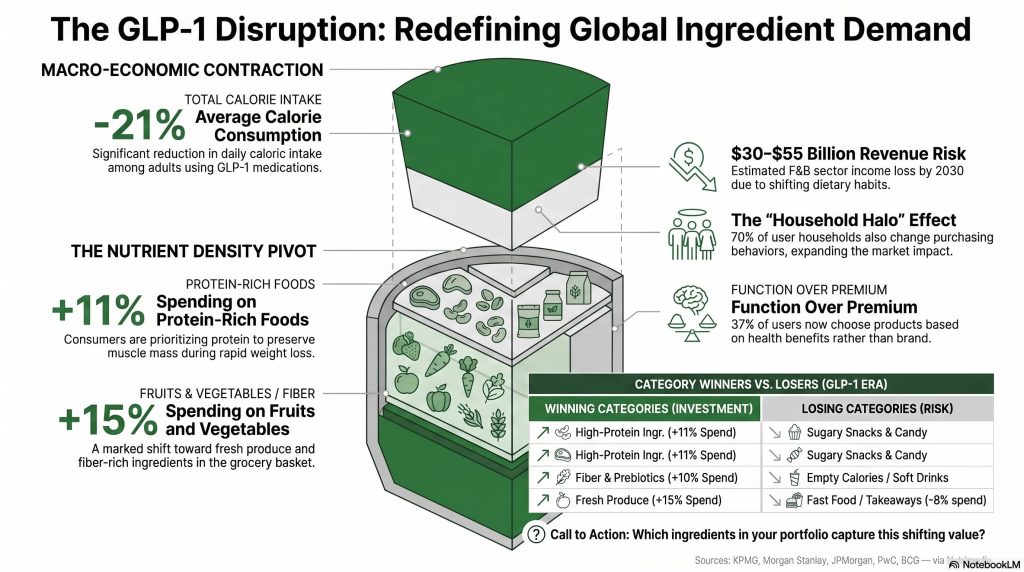

The GLP-1 users are eating less but better: an average of 21 % fewer calories, according to KPMG, and a shift in their diet towards protein, fruit and vegetables. For suppliers of’protein ingredients, it's a demand signal that is being redrawn in real time.

GLP-1 medications — Angonistes des récepteurs du Glucagon-like peptide-1, a satiety hormone (Ozempic, Wegovy and their competitors) — reduce appetite and alter what consumers buy. JPMorgan estimates that these treatments could cost the food and beverage sector £30 billion to £55 billion in annual revenue by 2030. The contraction particularly affects empty calories; demand for protein ingredients, in fibre and with higher nutritional density, it is progressing. For R&D and marketing managers in nutrition, the question is no longer whether this shift will happen, but which categories of ingredients will capture the value – and which will lose it.

What do GLP-1 medication consumption data actually measure?

The figures are all pointing in the same direction: less volume, more nutritional quality. Several analyses published in recent months document this.

- –21 % calories consumed on average by adults on GLP-1 medications, according to a KPMG analysis cited by CNBC.

- –3 to –4 % of grocery expenses for households with at least one user, and –7 to –9 % for single-person households, according to a PwC study reported by USA Today.

- +15 % of spending on fruit and vegetables and +11 % in protein-rich foods, according to Morgan Stanley.

- In South Africa, the SpendTrend26 report from Discovery Bank and Visa indicates that 48 % users of GLP-1 medications have reduced their spending on takeaways and dining out, while 59 % spend more on healthier food.

These figures illustrate a fact: when calorie intake is reduced, the user seeks to maintain their intake of protein and micronutrients. In other words, every remaining calorie has to «work» harder. This is where the protein ingredients and nutritional density become formulation drivers, not options.

Why are some restaurant chains revising their menus?

The industry response has been swift. According to NBC News, GLP-1 drugs are «normalising smaller appetites and higher protein intake» in dining out. Brands are translating this finding into menus.

| Teach | Documented response |

|---|---|

| Chipotle | «High-Protein Menu» featuring dishes containing between 15 and 81 g of protein |

| Shake Shack | High-protein, low-carbohydrate menu targeting GLP-1 users |

| Olive Garden (Darden) | Reduced portion sizes planned for 2026 following tests the previous autumn |

| Starbucks | Protein-rich lattes and small breakfast portions suitable for a reduced appetite |

The shift is twofold: less volume per portion, more protein per portion. For ingredient suppliers, this means demand is shifting towards protein ingredients high purity and organoleptic neutrality — capable of increasing content without increasing the format or degrading the taste.

The structural loser: low-nutrient-density foods

The Acosta Group study published in April notes that users of GLP-1 medicines buy more fresh, protein-rich foods and cut down on their purchases of sweets, savoury snacks and sugary drinks. The categories most affected by the $30–55 billion decline estimated by JPMorgan are precisely those with low nutritional density.

What ingredients will capture the recomposed demand?

The shift benefits three functional families: proteins (animal and vegetable), fibres, and foods with a high nutrient density – that is, a high nutrient-to-calorie ratio.

- Proteins high-solubility isolates and concentrates, required to achieve the 15 to 81 g per portion observed on the Chipotle menu without denaturing the texture.

- Fibres : to promote a feeling of fullness and aid digestion – a key consideration for users with a reduced appetite.

- Nutritional density : micronutrients and fortified formulations, to ensure adequate intake despite a reduction in the volume consumed.

The report Food Habits Landscape The Consumer Goods Forum, carried out with Bain & Company, identifies GLP-1 drugs as a force reshaping dietary decisions in Europe and the United States. For nutrition players, time is of the essence: the user base for GLP-1 drugs will continue to expand.

What this means for formulators

Three concrete projects. Premier : rethinking the protein-to-calorie ratio. With a reduction of 21 % in calorie intake (KPMG), a product must provide more protein and micronutrients per reduced portion — nutritional density becomes the key design criterion, not a secondary consideration.

Second master the organoleptic properties of protein ingredients At a high dose. Achieving 30 or 80 g of protein per item without bitterness or a sandy texture is key to adoption.

Third : incorporate fibre to promote satiety and digestive comfort. The +11 % increase in protein expenditure and +15 % increase in fruit and vegetables (Morgan Stanley) point to a food basket in which every ingredient must justify its nutritional value.

The base effect: why expected widening amplifies the signal

A third of the savings made on food by users of GLP-1 medications are being redirected to other health and wellness categories (clothing, wellness products), according to analysts cited by LinkedIn. The behaviour therefore goes beyond just diet.

Above all, Medicare must start covering GLP-1 medications for weight loss via a gateway programme from July 2026, according to the Content Management System. Mechanically, the user base is expanding, and with it the scope of the effects on demand. For suppliers of’protein ingredients, the repositioning window is before this extension, not after. The brands that have moved – Chipotle, Shake Shack, Olive Garden, Starbucks – have already understood this.

References

- The Consumer Goods Forum & Bain. (2026). State of Food Habits: A Baseline of How Consumers Eat Today. The Consumer Goods Forum.

- Bain & Company. (2026). Helping Consumers Make Healthier Choices. Bain & Company.

- Today Africa. (2026). Discovery Bank & Visa SpendTrend26: How weight-loss drugs are changing South African spending. Today, Africa.

- USA Today. (2026). GLP-1 users’ shopping behaviours (PwC research). USA Today.

- CNBC. (2026). GLP-1 diets, restaurants, protein and fibre (KPMG). CNBC.

- Morgan Stanley. (2026). Medicines and Changing Consumer Behaviour. Morgan Stanley.

- Supermarket News. GLP-1 drugs reshape consumer spending, eating and wellness habits (Acosta report). Supermarket News.

- NBC News. (2026). Smaller portions, more protein: how GLP-1s are quietly changing chain restaurants. NBC News.

- CMS. (2026). Medicare GLP-1 coverage (BALANCE transitional model, July 2026). Centres for Medicare & Medicaid Services.

FAQ

Are GLP-1 drugs an American phenomenon or a global signal?

Primarily American for now – the United States accounts for the majority of active prescriptions. But the signal is spreading. The SpendTrend26 report by Discovery Bank and Visa already documents changes in eating habits in South Africa, and the Consumer Goods Forum identifies a reshaping of food decisions in Europe. Scheduled Medicare coverage from July 2026 (CMS) will broaden the US user base, amplifying the effects on global ingredient supply chains.

What is the difference between an isolate and a concentrate of protein in this context?

One isolate generally contains more than 90 % of protein on a dry matter basis; a focused, between 60 and 80 %. To meet the targets of 30 to 80 g of protein per reduced-size portion observed at Chipotle, isolates — which offer high solubility and have a minimal impact on flavour and texture — are technically preferable. Concentrates remain suitable in formats where total calorie intake is not the limiting factor.

Which product categories are most exposed to declining demand?

According to the Acosta Group study, the purchases that are declining the most are confectionery, savoury snacks, and sugary drinks. These are precisely the categories with low nutritional density — abundant calories, and virtually no protein or micronutrients. JPMorgan estimates the overall sector decline to be between $30-55 billion in annual revenue by 2030 for the food and beverage sector as a whole.

Should an ingredient supplier explicitly target GLP-1 medication users in their B2B communication?

Not necessarily as a named segment. What the data shows is a structural shift towards nutritional density and protein – irrespective of the end consumer's purchasing motivation. For a supplier, the relevant argument is functional: an ingredient that allows one to achieve 30g of protein in a reduced format, without organoleptic compromise, meets a real formulation constraint, whether it’s linked to GLP-1 or not.

Are GLP-1 users exposed to specific nutritional deficiencies?

This is a well-documented risk. With a calorie intake of –21 % (KPMG), a sub-optimal diet can quickly lead to deficiencies in protein, iron, calcium, vitamin B12 and zinc — nutrients that are already under-consumed in the general population. A review published in Obesity Reviews in 2024 highlights that long-term GLP-1 users present a risk profile comparable to patients post-bariatric surgery regarding these micronutrients. For formulators, this is a direct lever: designing products with high nutritional density is not just a marketing argument.